Why is a Robust Field Network Crucial for Efficient Merchant Onboarding?

In today’s digital world, businesses are increasingly relying on streamlined processes to attract, onboard, and retain new customers and partners. One of the most critical processes in this regard is merchant onboarding—particularly for businesses that rely on a network of external merchants to sell their products or services. Whether you’re dealing with e-commerce, payment gateways, or local service providers, the efficiency of your merchant onboarding process can make or break your business growth.

But how can you speed up and improve the merchant onboarding experience? The answer lies in a strong field network. This powerful tool can significantly enhance the Merchant Onboarding Service, especially in markets like Merchant Onboarding Services in India, where logistical challenges and geographical diversity can slow down the process. Let’s dive into how building and leveraging a robust field network can revolutionize your onboarding process.

What Is Merchant Onboarding, and Why Is It So Important?

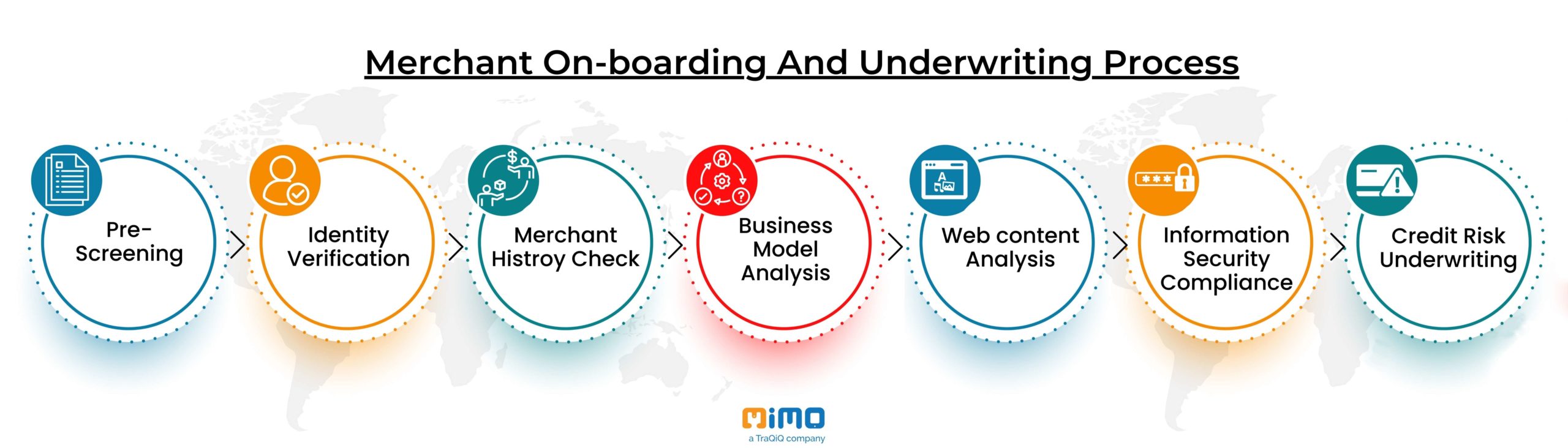

Before exploring how a strong field network can impact onboarding, it’s essential to understand what merchant onboarding entails. Merchant onboarding is the process of bringing new merchants into your ecosystem, setting them up with the tools they need to operate (such as software, payment systems, training, etc.), and integrating them into your business operations.

For any company looking to expand its reach and services, a smooth and efficient Merchant Onboarding Service is vital. The speed and efficiency with which new merchants are onboarded can directly influence revenue, customer satisfaction, and long-term partnerships. Especially in Merchant Onboarding Services in India, where a vast, diverse network of merchants is essential for growth, ensuring this process is seamless is crucial.

However, for businesses to onboard merchants effectively, they need more than just digital systems in place—they need a field service strategy that empowers local teams to engage directly with merchants in real-time, offering support, training, and troubleshooting as needed. This is where a field network becomes invaluable.

How Does a Strong Field Network Enhance Merchant Onboarding?

A field network refers to a system of local representatives, technicians, and customer support teams distributed across various regions who can interact with merchants on the ground. For a business looking to onboard merchants efficiently, having a strong field network provides several key advantages:

1. How Does Immediate Local Support Accelerate Onboarding?

When a merchant signs up to offer your services, they need to be guided through a complex array of tools and procedures—everything from setting up payment systems to understanding operational software and compliance regulations. Having field service teams available in the local area can significantly speed up this process.

Rather than relying on remote support, which can sometimes lead to communication delays and frustrations, a local field representative can provide hands-on assistance, troubleshoot problems, and ensure the merchant is fully equipped to get started quickly. This face-to-face support not only accelerates the process but also builds a personal connection, fostering trust and long-term partnerships with merchants.

For example, in Merchant Onboarding Services in India, where many merchants may have limited access to high-speed internet or remote support, in-person service becomes even more crucial. A field network ensures that local representatives can meet the unique needs of individual merchants, whether they’re in urban hubs or remote areas.

2. How Does Regional Expertise Improve Merchant Experience?

A strong field network brings local knowledge into the merchant onboarding process. This is especially helpful in a diverse country like India, where regional differences in culture, language, and business practices can be significant. A field service team with deep knowledge of the local market can help merchants navigate these differences effectively, ensuring a smoother onboarding experience.

Having representatives who understand the local business environment means that onboarding processes can be customized to fit each region’s specific needs. This level of personalization not only helps merchants feel more comfortable but also ensures that your product or service is integrated successfully with their existing processes.

For instance, a field representative in a remote village may offer insights into local payment preferences or help merchants who are unfamiliar with digital payment methods. On the other hand, in a metropolitan area, your field team can help streamline the setup process, ensuring that merchants quickly get up to speed with your systems and start making transactions without delay.

3. How Does the Speed of a Field Network Impact Merchant Onboarding?

A field network allows your business to react quickly to any roadblocks that might arise during the onboarding process. For instance, if a merchant faces challenges with the installation of software, setup of payment terminals, or understanding the operational system, a local representative can step in immediately to resolve the issue. This rapid response time minimizes delays and allows merchants to start selling faster.

In a typical Merchant Onboarding Service, delays caused by logistics, miscommunication, or technical issues can lead to frustrated merchants and slow down the onboarding process. However, by having a field network in place, these issues can be handled promptly, with local technicians and support teams available to resolve issues in real-time.

How Can a Field Network Improve Merchant Retention?

While onboarding is critical, retaining merchants is just as important. Onboarding may be quick, but to keep merchants engaged and satisfied, ongoing support is key. This is where the role of a field network truly shines.

1. How Does In-Person Interaction Build Trust and Loyalty?

Merchant relationships are built on trust. The more often your company can meet merchants in person and offer personalized support, the more likely they are to stay with your platform in the long term. A strong field network fosters loyalty by providing an ongoing, face-to-face connection with merchants.

By offering in-person visits for troubleshooting, upgrades, or even just check-ins, merchants feel that their needs are being heard and addressed. This not only makes them more likely to continue using your platform but also increases the likelihood that they will recommend your service to other potential merchants, expanding your network even further.

2. How Does Localized Support Increase Merchant Satisfaction?

Once a merchant is onboarded, they need continued support to ensure they’re maximizing the value of your service. A field network ensures that support isn’t just a phone call or email away—it’s a localized service that merchants can rely on for quick, real-world solutions. This kind of support is especially beneficial for merchants in areas where technical support might be sparse.

Having a field service team that provides consistent support means that merchants feel more confident in their decision to join your platform. They know they can rely on you not only during onboarding but throughout their entire relationship with your company.

What Are the Challenges of Building a Field Network for Merchant Onboarding?

While a field network offers numerous benefits, there are also some challenges to consider when building and maintaining one.

1. How Do You Scale a Field Network Across Multiple Regions?

One of the biggest challenges businesses face when building a field network is the ability to scale it effectively. Expanding your field service team across different regions requires strategic planning, hiring local representatives, and maintaining consistent training standards. As you grow your business and onboard more merchants in new areas, ensuring that your field team maintains high service standards becomes increasingly difficult.

However, with the right strategy—such as implementing a centralized management system for your field teams and using technology to track service quality and performance—you can successfully scale your field network to support merchant onboarding efforts across various regions.

2. How Do You Balance Cost and Coverage?

While a field network offers significant benefits, it also involves higher operational costs, such as travel expenses, salaries, and training. For businesses operating in diverse markets, balancing cost and coverage can be a delicate challenge. Efficient route planning, technology-driven tracking, and data analytics can help optimize field service costs, ensuring that you offer quality support without overextending your budget.

Conclusion: Why a Strong Field Network Is the Key to Efficient Merchant Onboarding

In conclusion, building a strong field network is essential for accelerating the merchant onboarding process. A field network brings in-person support, regional expertise, and rapid response times to your onboarding efforts, making it faster and more efficient. Whether you are operating in Merchant Onboarding Services in India or any other region, having a dedicated, localized field service team is key to ensuring your merchants get the best experience possible.

A well-structured field network doesn’t just help with onboarding—it also fosters long-term loyalty, builds trust, and ensures a successful merchant relationship. By investing in a robust field network, businesses can ensure faster, smoother onboarding and create lasting partnerships that drive growth and success.

About MIMO:

MIMO Technologies is a prominent FinTech and Digital Financial Services company that operates across various industries, providing technical solutions designed to accelerate business growth.

MIMO offers a wide range of services, including credit card and loan application processing, documentation handling, cheque and business document pickups, surveys and data collection, data digitization, background verification and screening, logistics, last-mile and hyperlocal delivery, transshipment, cash collection, document collection (NACH), and merchant onboarding.

In the background verification (BGV) sector, MIMO has successfully executed data collection across multiple domains and within strict timelines, thanks to its extensive PAN India network of field officers, data specialists, and a technology-driven platform. We help our clients connect with their target respondents and efficiently gather the data they need with ease.

Like this article?

More To Explore

What Is the Role of Background Checks in Establishing a Trustworthy Team?

+91 1141182211 One of the most vital assignments for any business is to bring in the right employees. Alongside skills

What Is a Last-Mile Strategy—And Why Is It Crucial for Your Business?

+91 1141182211 Ever ordered something online and then obsessively tracked the package as it made its way to your doorstep?

What Makes a PAN India Field Network Essential for Accurate Data Collection?

+91 1141182211 In today’s data-driven world, getting accurate, real-time insights from across the country is crucial for organizations that want