All

What Is the Role of Background Checks in Establishing a Trustworthy Team?

+91 1141182211 One of the most vital assignments for any business is to bring in the right employees. Alongside skills

The recent global health crisis has had an influence on a wide range of industries and geographies, not least the payments industry, which has seen an unprecedented transformation. Consumer purchasing habits have evolved to online shopping for products and services, resulting in the requirement for faster onboarding and better continuing merchant monitoring to reduce fraud and compliance risk for merchant acquirers.

When it comes to onboarding new merchants, automation is critical in order to make a smooth transition from the previous time-consuming approach to a slicker, faster process that reduces friction for the new merchant. But what steps should merchant acquirers take to guarantee that they are prepared to meet this new challenge of changing the customer experience while limiting risk?

It is critical for acquirers to provide a smooth merchant onboarding experience for their customers. With the epidemic hastening the general public’s shift to a more online approach, new smaller digital-only merchants are popping up all the time, with low margins and a need to be up and running quickly; for them, a swift onboarding procedure is vital.

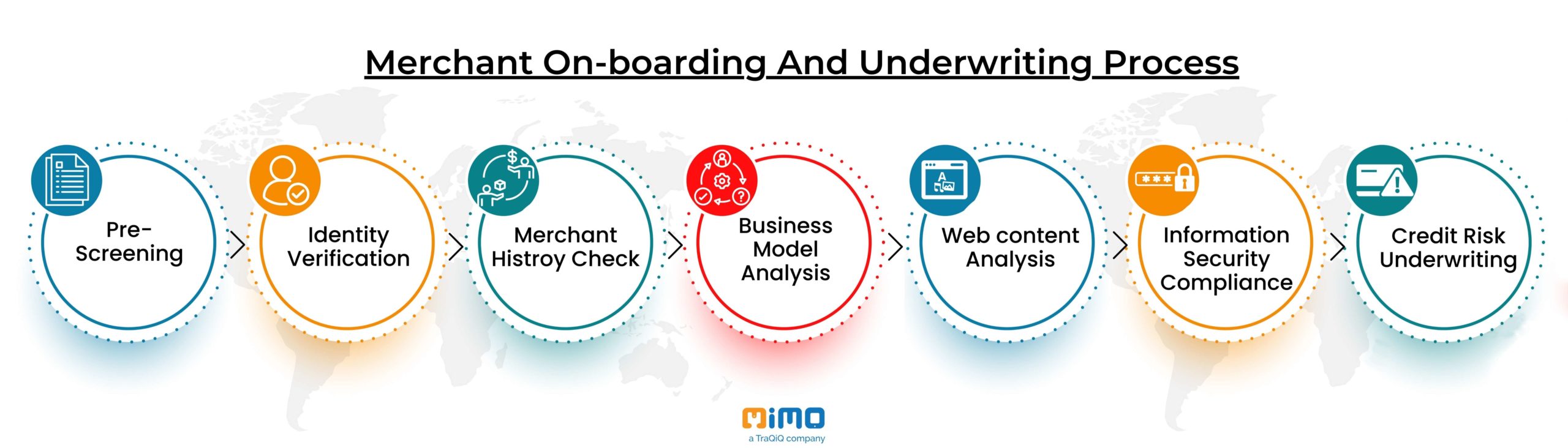

Before an underwriting decision can be made, the normal merchant onboarding process comprises a number of phases that must be completed, as shown in the creative below. This is typically a 3–5-day process. This process is too protracted, as previously said, given the current climate and the unique terrain of online-only micro-merchants.

Digital automation can shorten the time it takes to underwrite a new merchant from days to minutes. However, if not done appropriately, this speed in decision-making can come at the expense of risk management and have a detrimental influence on the acquirer’s profitability.

Effective onboarding decisioning requires access to meaningful and objective data. To enrich their perspective of each applicant, merchant acquirers should use a combination of their own data, third-party data, and assessment services. The best strategy is to combine application data with external data from a growing industry of data suppliers who can provide essential insight and assessment on topics like bank account validation, email addresses, IP addresses, device IDs, and negative hotlists. Internal data from various sources is ingested, which eliminates human data entry and reduces judgmental underwriting decisioning while also ensuring consistency.

Acquirers should not only have precise and objective data, but they should also be able to analyze it using analytic models and procedures. The tools should allow the acquirer to import models, scorecards, trees, and tables, and they should be completely user-configurable. Acquirers frequently have historical data about applicants in addition to external data, but it is inaccessible owing to the sprawl of data. Rather than going through the pain of trying to centralize all referential data in a single data store, design a solution that allows you to take data from multiple sources and retrieve it when you need it.

Risk management should not be the primary consideration for merchant acquirers and their merchant customers during the onboarding process. Merchant acquirers’ portfolios have become riskier as a result of increased digitization and demand for innovative payment options. As new entities pop up and enter the system at breakneck speed, the barrier to entry into the digital/ecommerce economy has increased. Validating these new entities necessitates the use of more robust systems that can make use of both internal and external data.

Acquirers should improve their ability to manage fraud and compliance risk by evaluating possible collusive or fraud-targeted merchant behavior, the chance of merchant attrition or insolvency, and current and prospective merchant profitability.

There is an increasing requirement for merchant monitoring in real-time in order to spot aberrant merchant behavior in time to prevent losses. We also find a lot of value in linking pre-book (onboarding) performance/results with post-book (monitoring) outcomes in order to establish a faster learning loop and enhance both areas. In reality, many acquirers are looking to meet both of these demands with a single platform/capability to improve insight sharing.

Risk management is a continuous necessity that does not end after a merchant is onboarded. The world of business moves quickly, and many businesses, particularly smaller, more flexible ones, must pivot or alter their course quickly to stay competitive. Their consumer profile may alter as a result of these developments. As a business grows, a merchant may need to expand into new markets or adjust the way they accept payments to accommodate a greater range of card types and payment methods. As a result, their risk profile may shift, leaving your company vulnerable.

Identifying potential changes in a merchant’s sales operations that could influence their risk criteria requires some type of ongoing monitoring. Keeping note of indicators such as surges in sales activity, surpassing payment thresholds, out-of-area or strange sales activities, and altering website products or connections can provide you with an up-to-date image of each merchant you work with and show any potential red flags. Keeping a lookout for their presence on punishment lists, as well as any unfavorable or adverse media coverage, will be essential.

An effective merchant monitoring approach will be automated, leverage cutting-edge analytics, real-time urgency and flexible data ingestion, and be able to proactively alert acquirers to potential risks and double as a competitive advantage for attracting new merchants to their network.

It’s critical to get your relationship with your new merchant off to the greatest possible start. A quick and flawless automated sign-up procedure can help attract and secure new merchants to your payments firm, but if things go wrong once they’ve signed on the dotted line, all your efforts could be for naught. A key component of the merchant onboarding process is a faster merchant setup. It enables merchants to swiftly deploy the equipment and technology they require to accept payments right now. As a result, this step should be as simple and straightforward as signing up.

Your new merchant will be a happy customer if everything is ready to ‘plug and play’ right out of the box. If it’s difficult to set up and get ready to use, they’ll toss it in the back of the drawer before it’s even used – and your brand’s reputation suffers as a result. As a result, make sure that all of the software, training materials, and other information that the merchant will need to get up and running is preloaded or supplied with the device, so that your new customer has everything they need right away.

Because of the ecommerce boom, the introduction of smart technology, and the pervasiveness of social media, today’s consumers demand fast access. This puts pressure on merchants and brands to be available to their customers 24 hours a day, seven days a week, which necessitates collaboration with service providers that can assist them in achieving this high level of service. Merchants, like customers, don’t want to wait weeks for a new potential payment provider to process their manual (or even paper) application. They expect to be up and running in a matter of minutes. Why not a merchant account if they can obtain this level of service with a commercial banking account?

To learn more about our advanced merchant onboarding solutions.

Like this article?

More To Explore

What Is the Role of Background Checks in Establishing a Trustworthy Team?

+91 1141182211 One of the most vital assignments for any business is to bring in the right employees. Alongside skills

What Is a Last-Mile Strategy—And Why Is It Crucial for Your Business?

+91 1141182211 Ever ordered something online and then obsessively tracked the package as it made its way to your doorstep?

What Makes a PAN India Field Network Essential for Accurate Data Collection?

+91 1141182211 In today’s data-driven world, getting accurate, real-time insights from across the country is crucial for organizations that want